1. Introduction to Artificial Intelligence in Accounting

Artificial Intelligence (AI) simulates human intelligence in machines, excelling in learning, reasoning, and self-correction. Key features include machine learning, natural language processing, automation, cognitive computing, and data analysis. AI’s evolution began in the 1950s, progressing through expert systems, machine learning, and deep learning, now impacting healthcare, finance, and retail significantly.

In accounting, AI is crucial due to data complexity, enhancing data handling, automating repetitive tasks, and improving decision-making. AI transforms accounting by streamlining routine tasks, enabling real-time financial monitoring, detecting fraud, ensuring tax compliance, providing predictive analytics, and enhancing auditing processes.

AI is revolutionizing accounting, increasing efficiency, and accuracy, and allowing professionals to focus on strategic activities.

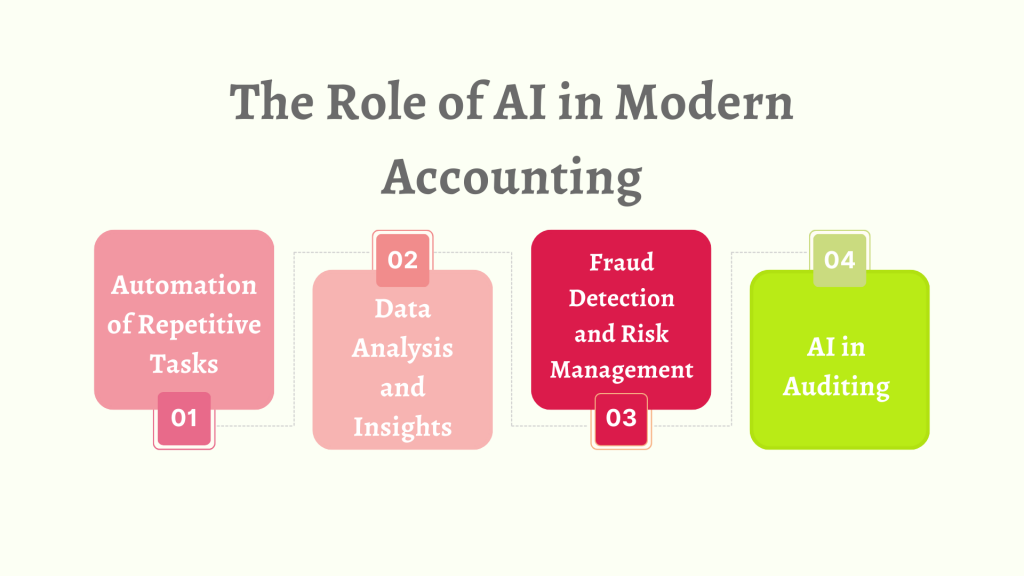

Artificial Intelligence (AI) is playing a transformative role in modern accounting by automating manual tasks, analyzing vast amounts of financial data, enhancing fraud detection, and improving audit processes. This section explores how AI technologies are reshaping the accounting landscape to make it more efficient, accurate, and data-driven.

Automation of Repetitive Tasks

Accounting involves a wide range of repetitive tasks that, while necessary, are time-consuming and prone to human error. AI excels at automating these processes, freeing up accountants to focus on higher-level analytical and advisory roles.

How AI Automates Tasks Like Data Entry, Reconciliations, and Bookkeeping:

Data Entry Automation: AI-driven systems can automatically extract information from invoices, receipts, and financial documents, inputting it directly into accounting software. This eliminates the need for manual data entry, reducing errors and saving time.

Reconciliation Processes: Bank reconciliations and general ledger reconciliations, which traditionally require manual matching of transactions, can now be automated with AI. AI systems compare financial records, flag discrepancies, and ensure that transactions are correctly recorded, vastly speeding up the reconciliation process.

Bookkeeping Automation: Routine bookkeeping tasks, such as categorizing transactions, tracking expenses, and generating financial statements, can be handled by AI-powered tools. These tools learn from historical data to categorize new transactions accurately and help maintain up-to-date financial records without human intervention.

Impact on Accounting:

Increases efficiency by drastically reducing the time required for routine tasks.

Minimizes human errors, ensuring more accurate and reliable financial records.

Allows accounting professionals to focus on strategic tasks like financial analysis, forecasting, and advisory services.

Data Analysis and Insights

In the era of big data, AI is an invaluable tool for analyzing vast amounts of financial information, detecting patterns, and uncovering insights that would be impossible or time-consuming for humans to process manually. AI-powered analytics tools are transforming how accountants interact with financial data.

Leveraging AI for Advanced Data Analytics and Generating Actionable Insights:

Pattern Recognition: AI algorithms are capable of identifying patterns and trends in financial data that may not be immediately apparent to human accountants. This allows for more accurate financial forecasting and strategic decision-making.

Predictive Analytics: AI can predict future financial trends based on historical data, helping organizations with budgeting, cash flow forecasting, and investment planning. This helps businesses anticipate financial risks and opportunities before they arise.

Real-Time Insights: AI-driven tools provide real-time insights into financial performance. By continuously monitoring data, AI systems can identify potential issues such as cash flow shortages or overspending early, enabling corrective action before these problems escalate.

Enhanced Reporting: AI can automatically generate detailed financial reports, offering actionable insights to business leaders in easily digestible formats such as dashboards, charts, and graphs.

Impact on Accounting:

Enhances decision-making with accurate, data-driven insights.

Enables more informed financial planning and strategy development.

One of AI’s most powerful applications in accountingis its ability to detect and prevent fraud. AI-driven systems can analyze transactional data, flag anomalies, and identify patterns of behavior that may indicate fraudulent activity.

Use of AI for Identifying Anomalies, Reducing Human Errors, and Detecting Fraud:

Anomaly Detection: AI systems can automatically detect irregularities in large datasets by recognizing deviations from normal patterns. For instance, unusual transaction amounts, unexpected vendors, or duplicate entries can be flagged for review, reducing the risk of fraud going unnoticed.

Continuous Monitoring: Unlike traditional audits, which typically occur at specific intervals, AI can provide continuous monitoring of financial transactions. This allows for real-time identification of suspicious activities and quicker intervention to prevent fraud.

Risk Assessment: AI tools can assess the financial health of a business, identifying areas that are more susceptible to risk. By analyzing factors like payment history, credit scores, and market conditions, AI helps businesses mitigate risks before they become major problems.

Impact on Accounting:

Significantly reduces the risk of financial fraud and errors.

Improves the overall security of financial systems and processes.

AI in Auditing

Auditing is another area of accounting that has greatly benefited from AI technologies. Traditional audits often require extensive manual reviews of financial data, which can be time-consuming and prone to oversight. AI is changing this by automating many aspects of the audit process, enhancing both speed and accuracy.

How AI Enhances Audit Processes, Making Them Faster and More Accurate:

Automated Data Review: AI can automatically review vast amounts of financial data, cross-referencing documents and identifying inconsistencies or irregularities. This allows auditors to focus their attention on areas that require deeper analysis rather than performing repetitive data checks.

Enhanced Accuracy: AI tools reduce the likelihood of human errors during audits, as they are capable of meticulously analyzing datasets with consistency and precision. This leads to more accurate audit reports and fewer oversight issues.

Continuous Auditing: AI enables continuous auditing, where financial transactions are analyzed in real time rather than being reviewed periodically. Continuous auditing provides up-to-the-minute assurance of financial compliance and reduces the time spent on end-of-year or quarter-end audits.

Risk-Based Auditing: AI can also prioritize audits based on risk, focusing on areas more likely to contain errors or discrepancies. This targeted approach saves time and improves the audit's effectiveness.

Impact on Accounting:

Makes audits faster and more comprehensive, improving the reliability of financial statements.

Allows for continuous monitoring, reducing the need for periodic audits.

Enhances the accuracy and depth of audits, leading to better compliance and fewer errors.

Artificial Intelligence (AI) in accounting leverages several key technologies to enhance efficiency, accuracy, and decision-making. These technologies help automate tasks, analyze large datasets, and provide valuable insights, transforming traditional accounting practices. In this section, we will explore some of the most impactful AI technologies used in accounting today: Machine Learning (ML), Natural Language Processing (NLP), Robotic Process Automation (RPA), Cognitive Computing, and AI-powered Financial Bots.

Machine Learning (ML)

Machine Learning (ML) is a subset of AI that allows systems to learn from data, recognize patterns, and make decisions with minimal human intervention. In accounting, ML algorithms are particularly valuable for analyzing vast amounts of financial data, detecting trends, and forecasting future outcomes.

How Machine Learning Algorithms Are Used for Predictive Analytics in Finance:

Financial Forecasting:Machine learning modelscan analyze historical financial data, such as revenue trends, cash flow patterns, and market fluctuations, to predict future financial performance. This helps businesses anticipate potential risks and make data-driven decisions about budgeting, investment, and resource allocation.

Risk Assessment:ML algorithms can assess financial risks by analyzing factors like credit history, customer behavior, and market conditions. By identifying patterns that may indicate increased risk, businesses can take proactive steps to mitigate losses.

Expense Management:ML models can automatically categorize and track expenses, making it easier for businesses to manage costs and identify areas for potential savings. These algorithms can also detect anomalies in expense reports, reducing the likelihood of fraud.

Credit Scoring and Loan Assessment: In financial institutions, ML is used to assess creditworthiness by analyzing a wide range of variables, including credit history, income, and spending behavior. This allows lenders to make more accurate loan decisions.

Enables more accurate forecasting and decision-making.

Reduces manual intervention in analyzing large datasets.

Natural Language Processing (NLP)

Natural Language Processing (NLP) is a branch of AI that focuses on enabling machines to understand, interpret, and generate human language. In accounting, NLP is used to automate tasks related to text processing, such as report generation, extracting insights from unstructured data, and facilitating communication.

Automation of Report Generation and Extraction of Financial Insights from Unstructured Data:

Automated Report Generation: NLP can automatically generatefinancial reports by processing data from multiple sources, interpreting the results, and presenting them in readable formats. This streamlines the process of creating reports such as balance sheets, profit and loss statements, and tax filings.

Processing Unstructured Data: Financial professionals often deal with unstructured data, such as emails, contracts, and invoices. NLP can extract valuable insights from these documents, categorize them, and integrate them into accounting systems for further analysis. For example, NLP can automatically identify relevant financial information from contract documents or extract expense details from receipts.

Text and Sentiment Analysis: NLP can analyze large volumes of text, such as customer feedback, social media posts, or industry news, to understand sentiment and emerging trends. This information can help businesses adapt their strategies based on customer satisfaction or market shifts.

Impact on Accounting:

Reduces the time spent on manual report creation and data extraction.

Helps businesses gain insights from unstructured text data, such as emails or contracts.

Improves communication through automated language understanding tools.

Robotic Process Automation (RPA)

Robotic Process Automation (RPA) involves using software robots or "bots" to automate repetitive, rule-based tasks that do not require human decision-making. In accounting, RPA is a game-changer, automating time-consuming processes such as data entry, invoice processing, and tax filing.

Automating Repetitive Tasks Like Invoice Processing and Tax Filings:

Invoice Processing: RPA can automate the entire invoice processing workflow, from receiving invoices to matching them with purchase orders and approving payments. By automating this process, businesses can reduce errors, speed up approvals, and ensure timely payments to suppliers.

Tax Filings: Tax preparation and filing are often complex, time-sensitive tasks that require meticulous attention to detail. RPA can automate data collection from financial records, calculate tax obligations, and even file returns with the appropriate tax authorities. This reduces the risk of errors and ensures compliance with tax regulations.

Data Entry: RPA bots can automatically extract financial data from various sources, such as emails, receipts, and accounting software, and input it into relevant systems. This eliminates the need for manual data entry and reduces the likelihood of human errors.

Improves accuracy by minimizing human errors in data entry and processing.

Reduces the time spent on repetitive tasks like invoice management and tax filings.

Cognitive Computing

Cognitive computing refers to AI systems that simulate human thought processes. These systems use techniques such as machine learning, data mining, and NLP to mimic the way humans think and make decisions. In accounting, cognitive computing helps professionals analyze complex financial data, make decisions, and develop strategies.

How Cognitive Technologies Mimic Human Thought Processes for Decision-Making:

Decision Support Systems:Cognitive computing systems can analyze large datasets, identify trends, and provide recommendations for financial decisions, such as investment strategies or risk mitigation. These systems can mimic the reasoning process accountants use when evaluating options, helping businesses make more informed choices.

Contract Analysis:Cognitive AI systems can review complex contracts, identify key terms, and ensure compliance with legal and regulatory requirements. This reduces the need for manual contract review and ensures that businesses avoid legal risks.

Complex Problem Solving: Cognitive computing can tackle complex financial problems, such as multi-currency reconciliations, financial forecasting under uncertain conditions, or optimizing tax strategies. These systems learn from past data and continuously improve their ability to solve problems.

Enhances financial strategy development through advanced problem-solving capabilities.

Reduces manual analysis of complex contracts and compliance documents.

AI-Powered Financial Bots

AI-powered financial bots, such as chatbots and virtual assistants, are increasingly being used in accounting to assist with customer support, financial operations, and data management. These bots are capable of understanding and responding to human inquiries, providing real-time assistance to both customers and accounting teams.

Role of Chatbots and Virtual Assistants in Customer Support and Financial Operations:

Customer Support:AI-powered chatbots can handle routine customer inquiries, such as questions about billing, payments, or account balances. They can provide 24/7 support, reducing the need for human intervention and improving customer satisfaction.

Transaction Management:AI botscan automate simple financial tasks, such as approving expenses, processing refunds, or managing payment schedules. This streamlines workflows and reduces the burden on human accountants.

Impact on Accounting:

Enhances customer support with instant, AI-driven responses.

AI is revolutionizing accounting by providing numerous benefits that enhance overall business performance. From improving productivity to enabling better financial decision-making, AI's transformative impact is driving the future of the accounting industry. In this section, we explore the key benefits of integrating AI into accounting, including increased efficiency, enhanced accuracy, cost savings, improved decision-making, and scalability.

Increased Efficiency and Productivity

One of the most significant advantages of AI in accounting is the boost in efficiency and productivity. By automating repetitive, time-consuming tasks, AI allows accounting teams to focus on more value-added activities such as strategic planning and data analysis.

How AI Reduces Manual Workload and Improves Efficiency Across Accounting Teams:

Automation of Routine Tasks:AI automates tasks such as data entry, invoice processing, payroll management, and reconciliations. This reduces the time spent on administrative work, allowing accountants to focus on tasks that require judgment and critical thinking.

Faster Processing of Large Volumes of Data:AI tools can process vast amounts of financial data in seconds, significantly reducing the time needed for tasks such as financial reporting or audits. This speed is crucial for businesses with high transaction volumes.

Streamlined Workflow:AI-powered systems can automate entire workflows, from capturing data to generating financial reports. This minimizes delays caused by manual intervention and ensures that accounting processes are completed quickly and efficiently.

Impact on Accounting:

Reduces the burden of manual tasks on accounting teams.

Increases overall productivity by enabling accountants to focus on higher-value work.

Enhanced Accuracy and Reduced Errors

Accuracy is critical in accounting, as even small errors can lead to significant financial discrepancies. AI-driven systems are designed to minimize the risk of human errors by automating complex data processing tasks and improving overall data accuracy.

AI’s Ability to Minimize Human Errors in Financial Data Processing:

Elimination of Data Entry Errors: Manual data entry can result in typos, incorrect entries, or inconsistent data. AI automates the process, ensuring accurate and consistent data input, and reducing the risk of mistakes.

Real-Time Error Detection: AI systems can monitor financial transactions in real time and flag potential errors or anomalies. This allows accountants to address issues as they arise, preventing them from escalating into larger problems.

Improved Audit Accuracy:AI tools used in audits can analyze vast amounts of data to identify discrepancies or inconsistencies, which human auditors might overlook. This enhances the accuracy of audits and reduces the likelihood of compliance issues.

Impact on Accounting:

Improves data accuracy, reducing the risk of costly errors.

Enhances the reliability of financial reports and audits.

Ensures that financial transactions and records are consistent and error-free.

Cost Savings

By automating time-intensive tasks and reducing the need for manual labor, AI contributes to significant cost savings for businesses. These savings can come from reduced staffing needs, fewer errors requiring correction, and the elimination of inefficiencies in the accounting workflow.

Reduced Operational Costs Through AI Automation:

Lower Labor Costs: With AI handling repetitive tasks, businesses can reduce the number of personnel required for basic accounting operations. AI tools can perform the work of multiple employees, allowing companies to reduce overhead without sacrificing output.

Fewer Correction Costs: Errors in financial records can be costly to fix, both in terms of time and resources. AI’s ability to reduce errors lowers the potential for these correction costs, saving money in the long run.

Streamlined Operations: Automating processes such as invoice management, payroll, and expense tracking reduces the need for costly manual interventions. This ensures that operations run smoothly, cutting down on wasted resources and time.

Impact on Accounting:

Reduces labor costs by automating manual tasks.

Decreases the financial impact of errors and corrections.

Improves overall operational efficiency, resulting in lower operational costs.

Improved Decision-Making

AI's ability to analyze large datasets and extract actionable insights empowers accountants and business leaders to make more informed financial decisions. AI-driven analytics help identify trends, predict future outcomes, and provide valuable recommendations for financial planning.

How AI-Driven Insights Empower Accountants to Make Better Financial Decisions:

Advanced Data Analytics: AI tools can analyze historical financial data and detect patterns that may not be visible through traditional methods. This allows businesses to anticipate market trends, customer behavior, and financial risks, leading to better decision-making.

Real-Time Reporting: AI systems provide real-time financial data and insights, enabling accountants to make decisions based on the most up-to-date information. This is especially important in fast-paced industries where financial decisions need to be made quickly.

Predictive Insights: AI can predict future financial scenarios, such as cash flow projections or potential risks, by analyzing historical data and identifying key variables. This foresight allows accountants to make proactive decisions, improving overall financial planning.

Impact on Accounting:

Enhances decision-making by providing accurate, real-time insights.

Enables businesses to make data-driven financial strategies.

Improves long-term financial planning and risk management.

Scalability and Flexibility

AI offers businesses the ability to scale their accounting operations without a significant increase in costs. As a company grows, its financial processes become more complex, requiring more resources to manage. AI enables seamless scalability by automating these processes, making it easier for businesses to handle increased volumes of transactions and financial data.

Enabling Businesses to Scale Accounting Operations Without a Significant Increase in Costs:

Handling Increased Transaction Volumes: As businesses grow, so do their financial transactions. AI systems can handle large volumes of data with ease, ensuring that accounting processes remain efficient even as the workload increases.

Flexible Financial Solutions: AI-driven accounting systems are adaptable and can be customized to fit the unique needs of different businesses. Whether a company needs to automate payroll, tax filing, or financial reporting, AI tools can be scaled to meet these needs.

Support for Multi-National Operations: AI accounting tools are often equipped with features that support multi-currency and multi-jurisdictional operations. This makes it easier for businesses to expand into new markets without the need for significant changes to their accounting systems.

Impact on Accounting:

Provides the ability to scale financial operations without a proportionate increase in costs.

Ensures flexibility in handling growing transaction volumes and complexity.

Supports business expansion by providing adaptable, scalable accounting solutions.

AI has found numerous practical applications in the accounting industry, revolutionizing how financial tasks are handled. By automating routine tasks and enhancing complex financial processes, AI is reshaping payroll management, financial forecasting, tax compliance, expense tracking, and invoice processing. Below are some of the most common applications of AI in accounting.

AI for Payroll Management

One of the key areas where AI is making an impact is payroll management. Traditional payroll processing involves significant manual work, including calculating salaries, deductions, and taxes. AI automates these processes, ensuring accuracy and reducing the time spent on administrative tasks.

How AI Automates Payroll Processing and Employee Tax Calculations:

Automated Salary Calculations: AI systems can quickly and accurately calculate salaries based on employee hours, overtime, and other factors, reducing errors and manual intervention.

Real-Time Tax Calculation: AI tools can update tax rates automatically based on current legislation, ensuring that employees’ taxes are correctly calculated and compliant with regional regulations.

Timely Payments: AI-powered payroll systems can schedule and automate payments to employees, ensuring timely disbursement without manual oversight.

Impact on Accounting:

Reduces time spent on payroll processing.

Minimizes payroll errors, ensuring compliance with tax laws.

Ensures timely and accurate employee compensation.

AI in Financial Planning and Forecasting

Financial planning and forecasting are crucial for businesses to stay competitive and maintain a healthy cash flow. AI models enhance these processes by analyzing large datasets to forecast trends, plan budgets, and predict financial performance with greater accuracy.

Using AI Models to Forecast Financial Trends, Budget Planning, and Financial Performance:

Predictive Analytics for Cash Flow: AI uses historical data to predict future cash flow, helping businesses anticipate financial needs and manage liquidity.

Budget Optimization: AI tools can suggest optimal budgeting strategies by analyzing past performance, market conditions, and future forecasts.

Scenario Analysis: AI allows businesses to simulate various financial scenarios, providing a clearer understanding of potential risks and opportunities.

Impact on Accounting:

Improves the accuracy of financial forecasting and planning.

Enables businesses to make proactive financial decisions.

Reduces uncertainty by providing data-driven financial insights.

AI for Tax Compliance

Tax compliance is a highly regulated area that requires meticulous attention to detail. AI simplifies tax compliance by automating processes related to tax filings, deductions, and adherence to regulatory frameworks.

Automation of Tax Filings, Deductions, and Compliance with Regulatory Frameworks:

Automated Tax Filings: AI can generate and file tax documents automatically, reducing the time accountants spend on tax preparation.

Real-Time Tax Law Updates: AI tools can track changes in tax laws and adjust filings to ensure compliance with new regulations.

Deductions Optimization: AI systems can identify deductions and credits that businesses might otherwise overlook, helping reduce overall tax liabilities.

Impact on Accounting:

Simplifies and automates tax filing processes.

Enhances compliance with ever-changing tax regulations.

Reduces the risk of penalties due to non-compliance.

Expense Management

Managing and analyzing company expenses is another key area where AI delivers value. AI-driven tools help businesses efficiently track, categorize, and monitor expenses, providing insights into spending patterns and opportunities for cost savings.

AI-Driven Tools for Tracking, Managing, and Analyzing Company Expenses:

Expense Categorization: AI can automatically categorize business expenses, ensuring that they are accurately recorded and aligned with company policies.

Real-Time Expense Monitoring: AI tools provide real-time insights into company spending, enabling businesses to manage their budgets more effectively.

Fraud Detection: AI systems can detect unusual or fraudulent expense claims by analyzing patterns and comparing them to typical spending behavior.

Impact on Accounting:

Streamlines expense tracking and management.

Provides real-time insights into business spending.

Reduces the risk of fraudulent expense claims.

AI in Invoice Processing

Manual invoice processing can be labor-intensive and prone to delays. AI automates invoice management, speeding up the process and reducing errors that can lead to payment delays or financial discrepancies.

Automating Invoice Management and Reducing Delays in Payment Processing:

Invoice Data Capture: AI tools automatically capture invoice details such as amounts, due dates, and vendor information, reducing manual data entry errors.

Payment Scheduling: AI systems can schedule payments based on invoice due dates, ensuring that vendors are paid on time and improving cash flow management.

Error Detection: AI can detect inconsistencies in invoices, such as duplicate entries or incorrect amounts, minimizing the chances of overpayment or missed payments.

Impact on Accounting:

Reduces manual effort in invoice processing.

Improves payment accuracy and prevents delays.

Enhances cash flow by ensuring timely payments.

6. Challenges and Risks of AI in Accounting

While AI offers substantial benefits, it also presents challenges and risks that businesses must address. Data privacy concerns, compliance issues, technology dependency, and the impact on jobs are critical areas that need careful consideration when integrating AI into accounting practices.

Data Privacy and Security Concerns

AI systems handle vast amounts of sensitive financial data, which makes them targets for cyberattacks. Ensuring the privacy and security of financial data is paramount when using AI in accounting.

Handling Sensitive Financial Data with AI and Ensuring Cybersecurity:

Data Encryption: AI systems must use advanced encryption techniques to protect financial data from unauthorized access.

Compliance with Data Protection Laws: AI-driven accounting tools must comply with regulations like GDPR or CCPA, ensuring that sensitive financial data is handled with care and stored securely.

Risk of Data Breaches: AI systems are susceptible to cyberattacks, and breaches can result in significant financial losses and reputational damage.

Ensuring AI systems comply with data privacy regulations and maintain secure data handling practices.

Compliance and Ethical Issues

AI must align with existing financial regulations and ethical standards. Failure to adhere to regulatory frameworks or ethical considerations could result in legal penalties or loss of trust.

Ensuring AI Aligns with Regulatory Standards and Ethical Considerations:

Regulatory Compliance: AI systems must comply with financial regulations such as Sarbanes-Oxley (SOX) or the International Financial Reporting Standards (IFRS).

Ethical Concerns: AI decisions, particularly in areas like auditing or tax compliance, must remain transparent and ethical, avoiding potential biases or conflicts of interest.

Ensuring AI tools are developed with transparency and fairness to maintain ethical standards.

Dependency on Technology

Over-reliance on AI systems can lead to vulnerabilities, especially if the technology fails or encounters a significant disruption.

Risks Associated with Over-Reliance on AI and Potential Disruptions:

System Downtime: If AI systems fail, accounting processes may come to a halt, potentially delaying financial reporting or payroll processing.

Lack of Human Oversight: Relying solely on AI without human intervention increases the risk of errors going unnoticed, especially in complex scenarios.

Mitigation:

Maintaining a balance between human oversight and AI automation to ensure that accountants still monitor critical tasks.

Having contingency plans in place in case of AI system failures.

Job Displacement Concerns

AI’s ability to automate accounting tasks raises concerns about job displacement within the industry. Accountants fear that AI may replace their roles, reducing job opportunities in the sector.

Addressing Fears of AI Replacing Human Accountants and the Need for Upskilling:

Shift Toward Higher-Value Roles: As AI takes over repetitive tasks, accountants can focus on more strategic activities such as financial analysis, consulting, and advising.

Upskilling: Accountants need to learn new skills related to AI tools, data analytics, and financial technology to remain competitive in the evolving industry.

Collaboration Between AI and Accountants: Rather than replacing human accountants, AI serves as a tool that enhances their capabilities, enabling them to work more efficiently and effectively.

Mitigation:

Encouraging continuous learning and upskilling in AI technologies for accountants.

Promoting AI as a complement to human expertise, not a replacement.

7. The Future of AI in Accounting

The future of AI in accounting promises to bring even more significant changes as emerging technologies continue to develop. From AI-driven platforms to the integration of blockchain, accounting will likely become more efficient, transparent, and insightful. Below are some key trends and predictions for the future of AI in accounting.

Emerging Trends in AI for Finance

The financial sector is rapidly adopting AI, and the coming years will see even more transformative developments.

The Rise of AI-Driven Accounting Platforms and Innovations to Watch:

AI-Enabled Accounting Software:Future accounting software will rely heavily on AI for automating complex processes such as financial forecasting, auditing, and compliance.

AI-Powered Virtual CFOs:AI tools may evolve into virtual financial officers, providing smaller businesses with access to high-level financial management services typically reserved for larger firms.

Cloud-Based AI Accounting:Cloud-based platforms will increasingly integrate AI for real-time financial analysis, offering businesses continuous access to financial insights.

As AI continues to handle routine tasks, accountants will experience a shift in their roles, moving away from traditional bookkeeping and toward more strategic positions.

Transition from Traditional Bookkeeping to More Strategic, Insight-Driven Roles:

From Data Entry to Data Analysis: Accountants will move beyond entering financial data to analyzing it and offering actionable business insights.

Advisory Services: With AI handling repetitive tasks, accountants will focus more on providing strategic consulting services, and advising on tax strategies, investments, and business expansion.

Enhanced Decision-Making: Accountants will collaborate closely with AI tools to interpret data and help businesses make data-driven decisions, positioning themselves as critical financial advisors.

Impact on Accounting Careers:

The role of accountants will shift from transactional to analytical and advisory.

Accountants will need to upskill in data analysis and financial technology to remain competitive.

AI’s Role in Real-Time Accounting

The concept of real-time accounting will become the norm as AI enables the continuous flow and analysis of data. This will revolutionize how financial information is processed, reported, and audited.

The Shift Toward Real-Time Data Processing and Continuous Auditing:

Real-Time Financial Reporting:AI will allow businesses to monitor their financial health in real-time, ensuring they are always up-to-date on cash flow, expenses, and revenue.

Continuous Auditing: AI will enable continuous auditing, where transactions are automatically checked for compliance and accuracy, reducing the need for periodic manual audits.

Instant Data Access:Real-time access to financial data will enable businesses to make quicker, more informed decisions, enhancing agility and competitiveness.

What to Expect:

Reduced time spent on financial close processes.

More frequent and accurate financial insights for better decision-making.

AI-driven auditing significantly reduces the risk of financial fraud.

AI Integration with Blockchain

Blockchain technologyand AI are set to converge, particularly in accounting, where the combination can offer enhanced security, transparency, and trust.

The Convergence of AI and Blockchain for Improved Transparency and Security in Accounting:

Enhanced Data Security:Blockchain’s decentralized ledger system ensures that financial transactions are securely recorded, while AI can analyze these transactions for accuracy and fraud detection.

Smart Contracts:AI, combined with blockchain, can manage and execute smart contracts automatically when pre-defined conditions are met, ensuring accurate and tamper-proof financial agreements.

Audit Trail Transparency: Blockchain provides an immutable audit trail, and AI can analyze these trails to identify irregularities and flag potential compliance issues, improving accountability in financial reporting.

Future Prospects:

AI and blockchain will make financial transactions more secure and trustworthy.

This integration will increase transparency, particularly in auditing and regulatory compliance.

8. Conclusion

AI is fundamentally transforming accounting through automation, real-time insights, and enhanced security. It improves efficiency and accuracy by minimizing errors and streamlining processes. As AI takes over routine tasks, accountants can focus on strategic activities, developing skills, and providing clients more value. The next decade will likely see AI influencing regulatory compliance, global financial integration, and ESG reporting. Embracing AI presents opportunities for growth and competitive advantage, making it essential for accountants to adapt to this technological shift. Overall, AI will drive innovation in financial processes, requiring continual adaptation from accounting professionals.

Revolutionize Your Accounting with AI-Driven Solutions

With cutting-edge tools such as Machine Learning, Natural Language Processing, and Robotic Process Automation (RPA), we help you streamline payroll management, tax compliance, and financial forecasting—all while reducing errors and operational costs.

Our AI-powered platforms also enhance your auditing and risk management capabilities, offering unmatched fraud detection and continuous auditing in real-time. Whether you’re a small business or a global enterprise, our AI-driven solutions will ensure that your financial operations are seamless, secure, and scalable.

Ready to Elevate Your Accounting with AI?

Contact us todayto discover how we can optimize your accounting processes with our innovative AI solutions. Let’s take your financial management to the next level!

Digital Marketing Specialist at Infiniticube, a leading app development and digital marketing agency in India. I specialize in B2B lead generation, AI-driven marketing solutions, and blockchain technology. Follow along for actionable insights on software trends and digital growth strategies for 2025 and beyond.

Our newsletter is finely tuned to your interests, offering insights into AI-powered solutions, blockchain advancements, and more. Subscribe now to stay informed and at the forefront of industry developments.

June 27, 2025

June 27, 2025

Balbir Kumar Singh

Balbir Kumar Singh

0

0

Leave a Reply