Decentralized Finance (DeFi) uses blockchain for financial services, offering accessibility, efficiency, transparency, innovation, and financial inclusion. Blockchain ensures decentralization, immutability, transparency, and security. DeFi revolutionizes finance by replacing intermediaries with decentralized networks.

The outline of this blog explains DeFi principles, innovations, advantages, challenges, real-world examples, and future trends. This blog aims to educate readers on DeFi's transformative potential in modern finance through blockchain technology, highlighting both its current state and future possibilities.

II. Background and Context

Traditional Financial Services

Centralized Banking Systems

Centralized banking systems have been the backbone of the global financial system for centuries. In a centralized banking system, financial institutions like banks, credit unions, and other financial intermediaries play a central role in facilitating and managing financial transactions. These institutions hold the authority to control the issuance of money, provide loans, accept deposits, offer investment products, and more.

Key Characteristics:

Central Authority: A central entity, such as a central bank or a regulatory body, oversees and regulates all financial activities.

Intermediation: Banks and other financial intermediaries act as middlemen between savers and borrowers, investors and markets.

Trust-Based System: Trust in these institutions and the regulatory frameworks that govern them is essential for the system's operation.

Common Services:

Deposits and Savings: Customers can deposit money into savings accounts and earn interest.

Lending and Borrowing: Banks provide loans and credit facilities to individuals and businesses.

Payments and Transfers: Facilitation of payments, money transfers, and currency exchange.

Investment Services: Offering investment products like stocks, bonds, and mutual funds.

Limitations and Challenges

Despite their long-standing role in the financial ecosystem, centralized banking systems have several limitations and challenges:

Accessibility and Inclusivity:

Unbanked Population: A significant portion of the global population remains unbanked or underbanked, lacking access to essential financial services.

Geographical Barriers: People in remote or underserved regions often face difficulties accessing banking services.

Efficiency and Costs:

High Transaction Fees: Intermediaries often charge substantial fees for transactions, particularly cross-border transfers.

Slow Processes: Traditional banking transactions, especially international ones, can be slow due to the involvement of multiple intermediaries and regulatory checks.

Transparency and Trust:

Opacity: Customers often lack visibility into the inner workings of banks and the status of their transactions.

Trust Issues: Financial crises and scandals have led to a loss of trust in traditional financial institutions.

Regulation and Control:

Centralized Control: Central authorities can impose restrictions, manipulate interest rates, and influence the money supply, which may not always align with the best interests of the public.

Regulatory Compliance: Stringent regulations can stifle innovation and make it difficult for new entrants to offer competitive financial products.

Emergence of Blockchain Technology

History and Development

Blockchain technology was first conceptualized in 2008 by an anonymous person or group known as Satoshi Nakamoto. The technology was introduced as the underlying infrastructure for Bitcoin, the first cryptocurrency, in Nakamoto's whitepaper titled "Bitcoin: A Peer-to-Peer Electronic Cash System."

Key Milestones:

2009: The Bitcoin network was launched, marking the first practical implementation of blockchain technology.

2011-2013: Other cryptocurrencies like Litecoin and Ripple emerged, showcasing blockchain's potential beyond Bitcoin.

2015: Ethereum was introduced, featuring smart contracts that allowed for the creation of decentralized applications (dApps).

2017: The rise of Initial Coin Offerings (ICOs) demonstrated blockchain's capability for fundraising and asset tokenization.

2019-Present: Increased interest from enterprises and governments in exploring blockchain applications for supply chain management, finance, healthcare, and more.

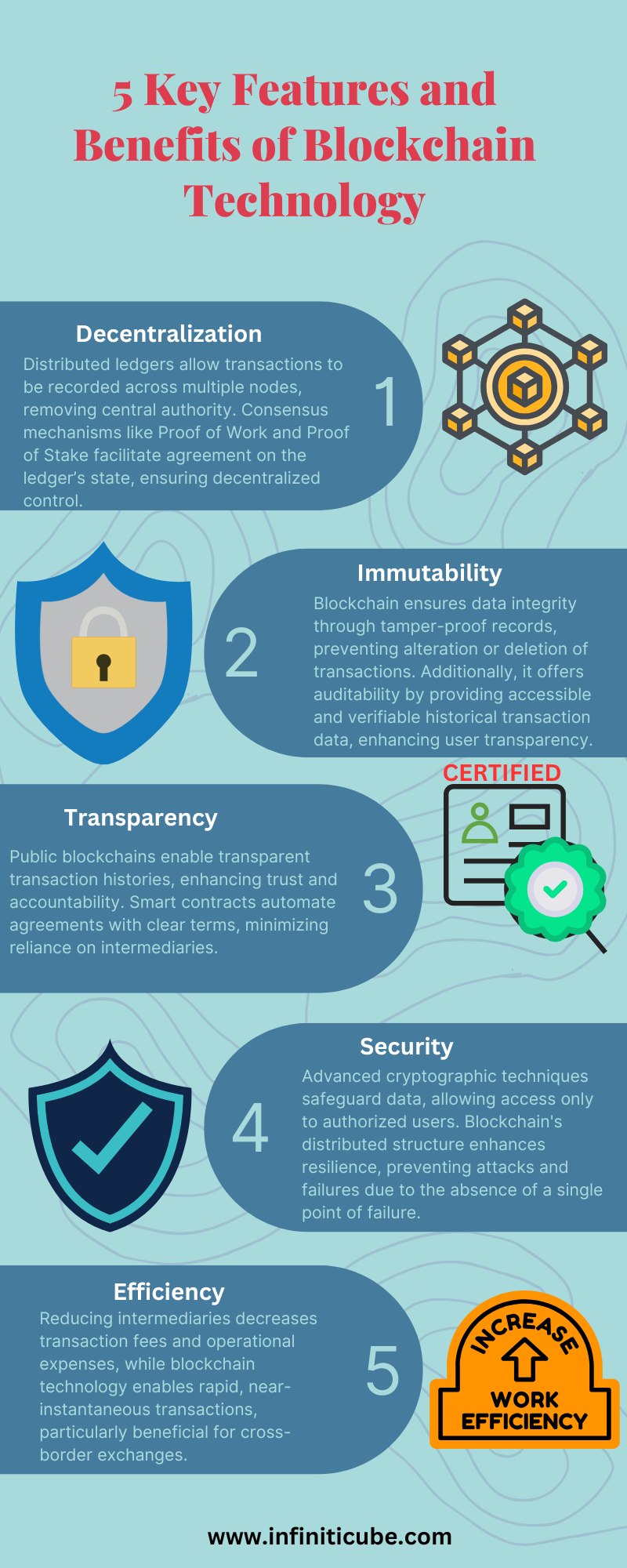

Key Features and Benefits

Blockchain technology offers several unique features and benefits that address many of the limitations of traditional financial systems:

Decentralization:

Distributed Ledger: Transactions are recorded across a network of computers (nodes), eliminating the need for a central authority.

Consensus Mechanisms: Various consensus protocols, such as Proof of Work (PoW) and Proof of Stake (PoS), ensure agreement on the ledger's state without central control.

Immutability:

Tamper-proof Records: Once a transaction is added to the blockchain, it cannot be altered or deleted, ensuring data integrity.

Auditability: Historical transaction data is accessible and verifiable by anyone, enhancing transparency.

Transparency:

Open Ledger: Public blockchains allow anyone to view transaction histories, fostering trust and accountability.

Smart Contracts: Self-executing contracts with transparent terms reduce the need for intermediaries and manual intervention.

Security:

Cryptographic Security: Advanced cryptographic techniques protect data and ensure that only authorized parties can access sensitive information.

Resilience: The distributed nature of blockchain makes it resistant to attacks and failures, as there is no single point of failure.

Efficiency:

Reduced Costs: Eliminating intermediaries lowers transaction fees and operational costs.

Faster Transactions: Blockchain can facilitate near-instantaneous transactions, especially in cross-border scenarios.

In summary, blockchain technology offers a robust alternative to traditional centralized financial systems by providing decentralization, immutability, transparency, security, and efficiency. These features have paved the way for the rise of Decentralized Finance (DeFi), which leverages blockchain to transform financial services.

III. Understanding DeFi

Core Principles of DeFi

Decentralization

Decentralization is the foundational principle of DeFi. Unlike traditional financial systems that rely on central authorities, DeFi operates on blockchain networks that are maintained by a distributed network of nodes. This decentralization eliminates the need for intermediaries such as banks and allows for peer-to-peer transactions.

Key Aspects:

Distributed Network: Transactions and data are stored across multiple nodes, reducing the risk of single points of failure.

Consensus Mechanisms: Protocols such as Proof of Work (PoW) or Proof of Stake (PoS) ensure that all network participants agree on the state of the blockchain, maintaining integrity and trust.

Benefits:

Reduced Central Control: No single entity can manipulate the system, leading to fairer and more democratic financial services.

Resilience: The distributed nature makes the network more resistant to outages and attacks.

Transparency

Transparency in DeFi is achieved through the open nature of blockchain technology. All transactions are recorded on a public ledger, allowing anyone to verify and audit them.

Key Aspects:

Public Ledger: Transaction data is visible to all network participants, enhancing accountability.

Open-Source Protocols: Many DeFi projects operate on open-source code, allowing anyone to review and contribute to the development.

Benefits:

Trust and Accountability: Users can independently verify the integrity of transactions and smart contracts.

Reduced Fraud: The transparent nature makes it difficult for malicious actors to conceal fraudulent activities.

Accessibility

DeFi aims to democratize access to financial services by removing barriers associated with traditional banking systems. Anyone with an internet connection can participate in DeFi.

Key Aspects:

Permissionless Systems: Users do not need approval from central authorities to use DeFi services.

Global Reach: DeFi platforms are accessible from anywhere in the world, provided there is internet connectivity.

Benefits:

Financial Inclusion: DeFi provides financial services to the unbanked and underbanked populations.

Lower Barriers to Entry: Reduced need for documentation and background checks enables more people to access financial services.

Key Components of DeFi

Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automatically enforce and execute the terms when predefined conditions are met.

Key Aspects:

Automation: Smart contracts eliminate the need for intermediaries by automating processes.

Security: The code runs exactly as programmed, reducing the risk of errors and tampering.

Benefits:

Efficiency: Automated processes reduce transaction times and operational costs.

Trust: Users can trust that the contract will execute as intended without human intervention.

Decentralized Applications (dApps)

Decentralized Applications (dApps) are applications that run on a blockchain network rather than a centralized server. They interact with smart contracts to offer various financial services.

Key Aspects:

Interoperability: dApps can interact with each other on the same blockchain, creating a seamless ecosystem of services.

User Control: Users retain control over their data and assets when using dApps.

Benefits:

Innovation: Developers can create and deploy a wide range of financial products and services.

User Empowerment: Users have greater control and ownership over their financial activities.

Tokenization and Cryptocurrencies

Tokenization refers to the process of converting real-world assets or rights into digital tokens on a blockchain. Cryptocurrencies are digital or virtual currencies that use cryptography for security.

Key Aspects:

Asset Representation: Tokens can represent a variety of assets, including currencies, commodities, real estate, and more.

Liquidity: Cryptocurrencies and tokens can be easily traded on decentralized exchanges (DEXs).

Benefits:

Fractional Ownership: Tokenization allows for the division of assets into smaller, more affordable units.

Enhanced Liquidity: Digital tokens can be traded 24/7, providing greater liquidity and market access.

In summary, the core principles of DeFi—decentralization, transparency, and accessibility—along with key components such as smart contracts, dApps, and tokenization, form the backbone of this innovative financial ecosystem. DeFi leverages blockchain technology to create a more open, efficient, and inclusive financial system.

IV. Innovations in DeFi Financial Services

Lending and Borrowing Platforms

Peer-to-Peer Lending

Peer-to-peer (P2P) lending platforms in DeFi allow individuals to lend and borrow directly from each other without the need for a centralized financial institution. These platforms use smart contracts to automate and secure the lending process, ensuring transparency and trust between participants.

Key Features:

Direct Interaction: Borrowers and lenders interact directly through the platform.

Flexible Terms: Lenders can set their own interest rates and terms.

Benefits:

Lower Costs: Eliminating intermediaries reduces fees and interest rates.

Greater Access: Individuals who may not qualify for traditional loans can access credit.

Transparency: All loan terms and transactions are recorded on the blockchain.

Collateralized Loans

Collateralized loans in DeFi require borrowers to provide digital assets as collateral to secure a loan. If the borrower defaults, the collateral is liquidated to repay the lender. This reduces the risk for lenders and allows borrowers to access funds without selling their assets.

Key Features:

Over-Collateralization: Borrowers must provide collateral worth more than the loan amount to account for market volatility.

Automatic Liquidation: Smart contracts automatically liquidate collateral if the borrower's collateral value falls below a certain threshold.

Flexible Assets: Various cryptocurrencies and tokens can be used as collateral.

Asset Retention: Borrowers can access liquidity without selling their digital assets.

Fast Processing: Loans can be approved and disbursed quickly through smart contracts.

Decentralized Exchanges (DEXs)

Automated Market Makers (AMMs)

Automated Market Makers (AMMs) are a type of DEX that uses algorithms to price assets and facilitate trading without needing an order book. Liquidity is provided by users who deposit their assets into liquidity pools.

Key Features:

Algorithmic Pricing: Prices are determined by a mathematical formula based on the ratio of assets in the liquidity pool.

Liquidity Providers (LPs): Users provide liquidity by depositing asset pairs into pools and earning fees from trades.

Constant Product Formula: Popular AMMs like Uniswap use the formula x*y=k to maintain balance in the pool.

Benefits:

Continuous Liquidity: AMMs provide liquidity at all times, regardless of trading volume.

Lower Barriers to Entry: Anyone can become a liquidity provider and earn fees.

Decentralized Trading: No need for centralized order matching.

Liquidity Pools

Liquidity pools are collections of funds locked in a smart contract that are used to facilitate trading on DEXs. Users (liquidity providers) contribute assets to these pools and earn a share of the trading fees generated.

Key Features:

Pooled Assets: Multiple users contribute assets to create a large pool that supports trading.

Fee Distribution: Fees generated from trades are distributed to liquidity providers based on their share of the pool.

Impermanent Loss: Liquidity providers face the risk of impermanent loss, where the value of their deposited assets may change relative to holding the assets outside the pool.

Benefits:

Enhanced Liquidity: Large pools enable significant trading volumes without price slippage.

Earnings Potential: Liquidity providers earn passive income from trading fees.

Decentralization: Liquidity pools operate without centralized control.

Stablecoins and Digital Assets

Types of Stablecoins

Stablecoins are cryptocurrencies designed to maintain a stable value, typically pegged to a fiat currency like the US Dollar. They provide stability and are widely used in DeFi.

Key Types:

Fiat-Collateralized: Backed by reserves of fiat currency held in a bank (e.g., USDC, Tether).

Crypto-Collateralized: Backed by other cryptocurrencies, often over-collateralized to account for volatility (e.g., DAI).

Algorithmic: Maintain stability through algorithmic mechanisms and smart contracts that adjust supply based on demand (e.g., TerraUSD).

Benefits:

Price Stability: Stablecoins offer a stable store of value and medium of exchange.

Integration: Easily integrated into DeFi platforms for lending, borrowing, and trading.

Accessibility: Provide an on-ramp for users to enter the crypto ecosystem without exposure to volatility.

Use Cases and Benefits

Stablecoins and digital assets play a crucial role in DeFi by providing stability, liquidity, and accessibility.

Use Cases:

Trading and Hedging: Stablecoins allow traders to hedge against volatility.

Remittances: Facilitate low-cost, fast cross-border transactions.

Savings and Payments: Used for savings accounts, payments, and as collateral in lending platforms.

Benefits:

Stability: Protects users from the volatility of other cryptocurrencies.

Liquidity: Enhances liquidity in DeFi markets and platforms.

Accessibility: Enables participation in DeFi for users without exposure to crypto volatility.

Yield Farming and Staking

Concepts and Mechanisms

Yield farming and staking are methods for earning rewards by participating in DeFi protocols.

Yield Farming:

Liquidity Mining: Users provide liquidity to DeFi protocols and earn rewards, often in the form of the protocol's native tokens.

Reward Mechanisms: Incentivizes users to lock up their assets, providing liquidity and stability to the platform.

Staking:

Proof of Stake (PoS): Users lock up their tokens to support network security and operations, earning staking rewards in return.

Delegated Staking: Users delegate their tokens to a validator who stakes on their behalf, sharing the rewards.

Mechanisms:

Smart Contracts: Automate reward distribution and ensure transparency.

APY (Annual Percentage Yield): Represents the potential annual return on staked or farmed assets.

Benefits:

Passive Income: Users earn passive income from their crypto holdings.

Network Security: Staking contributes to the security and stability of blockchain networks.

Yield farming and staking offer significant returns but come with inherent risks.

Potential Returns:

High APY: Yield farming can offer high returns, particularly in the early stages of a project.

Staking Rewards: Regular staking rewards provide a predictable income stream.

Risks:

Impermanent Loss: In yield farming, changes in the relative price of deposited assets can lead to losses.

Smart Contract Risks: Vulnerabilities in smart contracts can result in loss of funds.

Market Volatility: The value of rewards and staked assets can fluctuate, impacting overall returns.

Insurance and Risk Management

Decentralized Insurance Protocols

Decentralized insurance protocols provide coverage for various risks in the DeFi ecosystem. These protocols use smart contracts to automate the claims process and reduce the need for intermediaries.

Key Features:

Automated Claims: Smart contracts handle claims based on predefined criteria.

Coverage Options: Provide insurance for smart contract failures, exchange hacks, and other risks.

Mutual Insurance Models: Users pool their funds to share risk and receive compensation in case of claims.

Benefits:

Cost Efficiency: Lower premiums due to reduced administrative costs.

Transparency: Clear terms and automated claims enhance trust.

Accessibility: Wider access to insurance products for DeFi users.

Risk Mitigation Strategies

Effective risk management is crucial for participants in the DeFi ecosystem.

Strategies:

Diversification: Spreading investments across different DeFi projects to mitigate risk.

Audits and Security Reviews: Ensuring that smart contracts are audited by reputable firms.

Insurance Coverage: Utilizing decentralized insurance protocols to cover potential losses.

Staying Informed: Keeping up-to-date with the latest developments and potential risks in the DeFi space.

Benefits:

Reduced Exposure: Diversification and insurance reduce exposure to individual project risks.

Increased Confidence: Audits and security measures enhance user confidence in DeFi platforms.

Protection: Insurance provides a safety net against unforeseen losses.

In summary, DeFi innovations such as lending and borrowing platforms, DEXs, stablecoins, yield farming, staking, and decentralized insurance are transforming financial services. These innovations offer new opportunities for earning, trading, and managing risks while leveraging the benefits of blockchain technology.

V. Advantages of DeFi in Financial Services

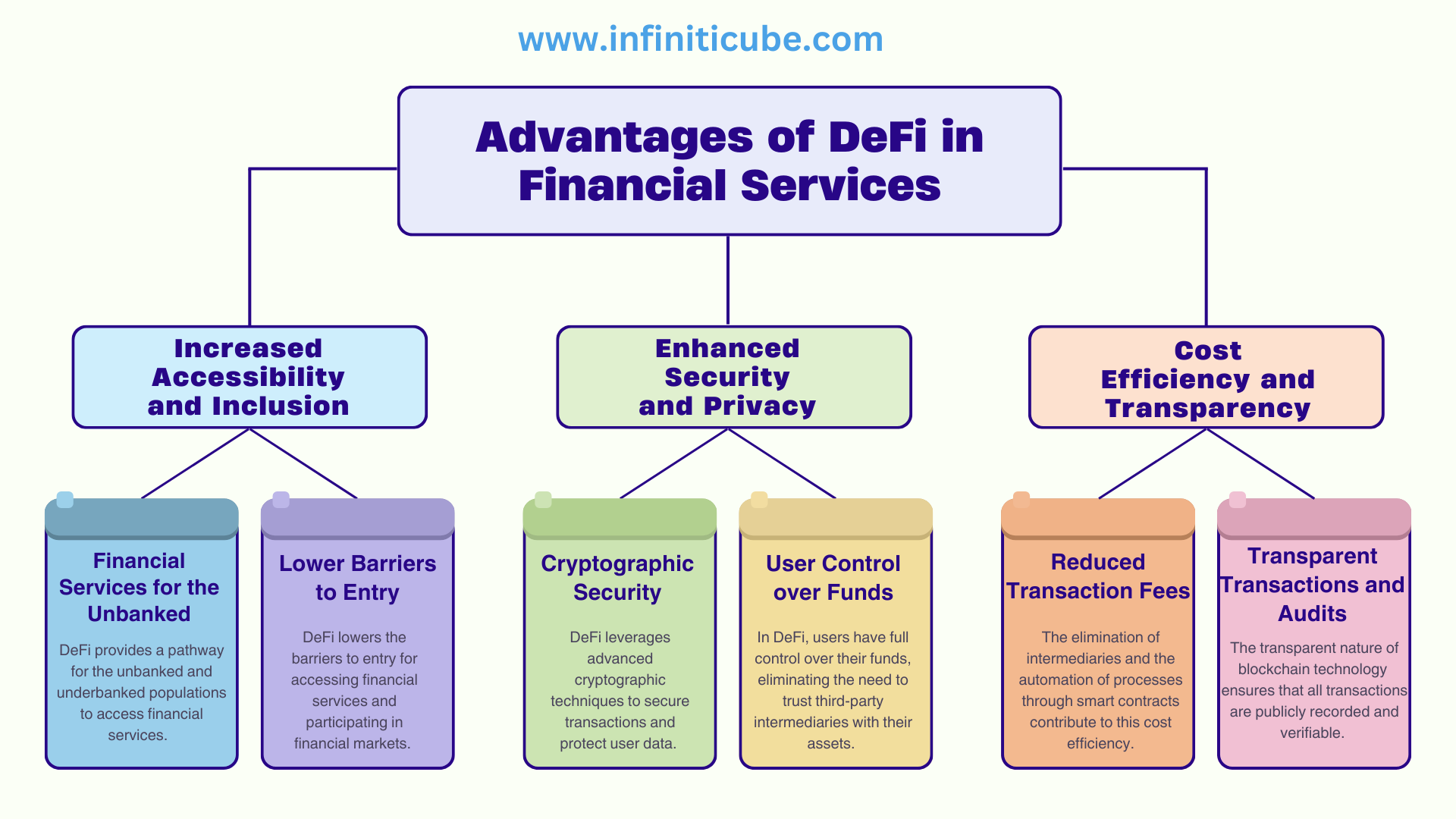

Increased Accessibility and Inclusion

Financial Services for the Unbanked

DeFi provides a pathway for the unbanked and underbanked populations to access financial services. Traditional banking systems often exclude individuals due to geographical, socio-economic, or bureaucratic barriers. DeFi eliminates these barriers by leveraging blockchain technology.

Key Points:

Global Access: Anyone with an internet connection can access DeFi platforms, regardless of their location.

No Need for Traditional Identification: DeFi platforms typically require only a digital wallet, making it easier for individuals without traditional identification to participate.

Benefits:

Empowerment: Provides financial tools to individuals who have been historically excluded from the traditional financial system.

Economic Opportunities: Enables the unbanked to save, invest, and borrow, fostering economic growth and financial independence.

Lower Barriers to Entry

DeFi lowers the barriers to entry for accessing financial services and participating in financial markets. Traditional financial systems often have high entry requirements, such as minimum account balances and extensive paperwork.

Key Points:

Ease of Access: Users can join DeFi platforms with minimal technical knowledge and financial investment.

Low Minimum Requirements: Many DeFi services do not require significant upfront capital, making them accessible to a wider audience.

Benefits:

Inclusivity: More people can participate in financial activities without facing prohibitive costs or requirements.

Diverse Participation: Attracts a broader demographic, including small investors and individuals from developing regions.

Enhanced Security and Privacy

Cryptographic Security

DeFi leverages advanced cryptographic techniques to secure transactions and protect user data. Blockchain technology ensures that data is immutable and transparent, reducing the risk of fraud and unauthorized access.

Key Points:

Encryption: Data and transactions are encrypted, ensuring that only authorized parties can access sensitive information.

Immutable Ledger: Once recorded, transactions cannot be altered, providing a permanent and tamper-proof record.

Benefits:

Data Integrity: Ensures the accuracy and reliability of transaction records.

Reduced Fraud: Cryptographic security makes it difficult for malicious actors to alter or forge transactions.

User Control over Funds

In DeFi, users have full control over their funds, eliminating the need to trust third-party intermediaries with their assets. This self-custody model enhances security and privacy.

Key Points:

Self-Custody: Users maintain ownership and control of their private keys, which are required to access their funds.

Permissionless Access: Users can engage with DeFi platforms without needing approval from a central authority.

Benefits:

Increased Security: Reduces the risk of hacks and mismanagement associated with centralized custodians.

Privacy: Users can transact without disclosing personal information to intermediaries.

Cost Efficiency and Transparency

Reduced Transaction Fees

DeFi platforms often have lower transaction fees compared to traditional financial services. The elimination of intermediaries and the automation of processes through smart contracts contribute to this cost efficiency.

Key Points:

No Middlemen: Direct peer-to-peer transactions reduce the need for intermediary fees.

Savings for Users: Lower fees make financial services more affordable, particularly for small transactions and microloans.

Increased Adoption: Cost efficiency attracts more users to DeFi platforms, driving growth and innovation.

Transparent Transactions and Audits

The transparent nature of blockchain technology ensures that all transactions are publicly recorded and verifiable. This transparency builds trust and allows for real-time audits.

Key Points:

Public Ledger: All transactions are recorded on a blockchain, accessible to anyone for verification.

Auditable: The open ledger allows for continuous auditing and monitoring of transactions and smart contracts.

Benefits:

Accountability: Transparent transactions reduce the risk of fraud and corruption.

Trust: Users can independently verify the integrity of transactions and the financial health of DeFi platforms.

In summary, DeFi offers significant advantages in financial services, including increased accessibility and inclusion, enhanced security and privacy, and cost efficiency and transparency. By leveraging blockchain technology, DeFi creates a more open, secure, and equitable financial system.

VI. Challenges and Risks in DeFi

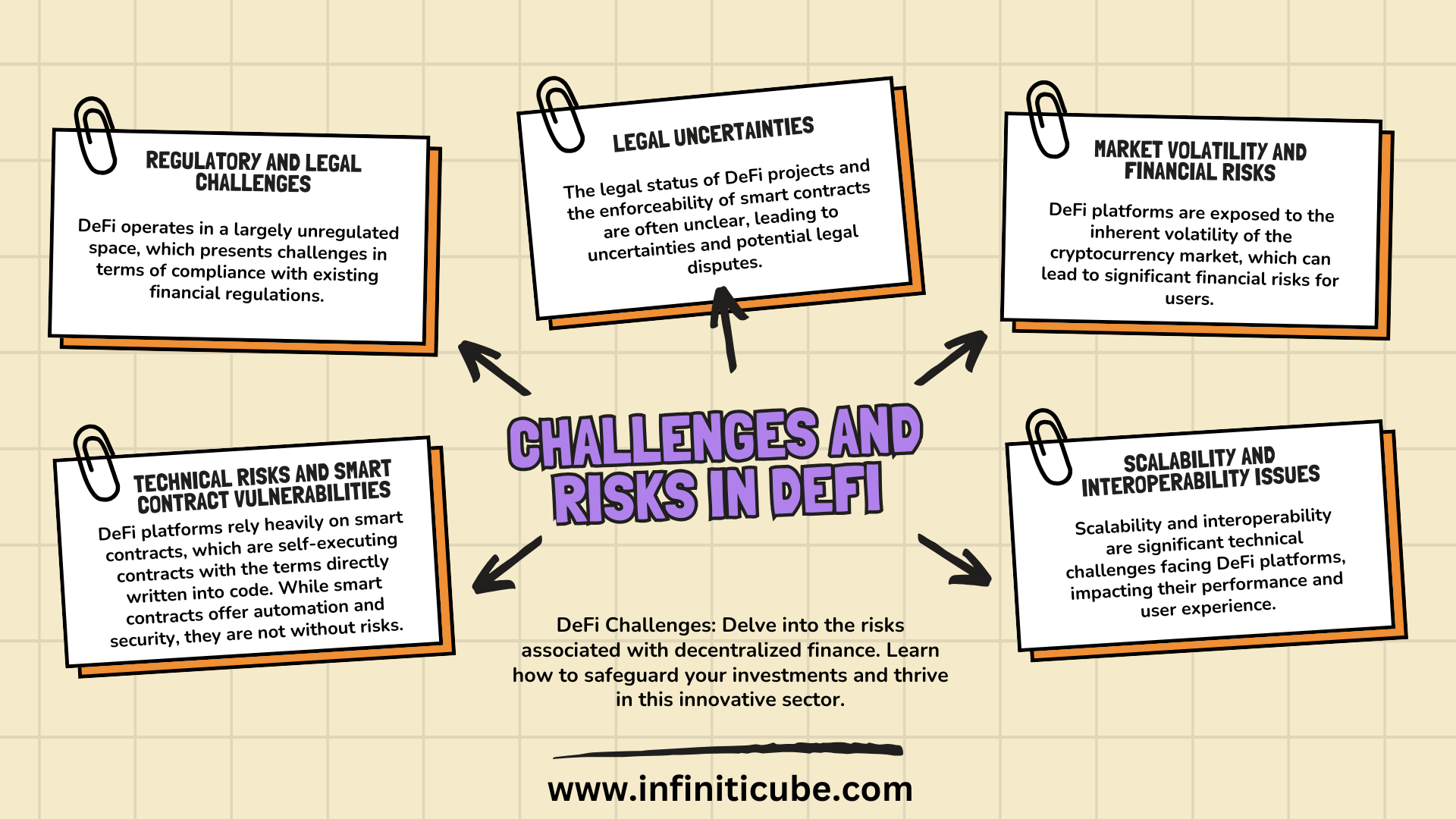

Technical Risks and Smart Contract Vulnerabilities

DeFi platforms rely heavily on smart contracts, which are self-executing contracts with the terms directly written into code. While smart contracts offer automation and security, they are not without risks.

Key Points:

Code Exploits: Vulnerabilities in smart contract code can be exploited by malicious actors, leading to loss of funds.

Bugs and Errors: Even minor coding errors can have significant consequences, potentially leading to unintended outcomes or system failures.

Audit Limitations: While third-party audits can help identify vulnerabilities, they are not foolproof and cannot guarantee complete security.

Examples:

DAO Hack: In 2016, a vulnerability in the smart contract of the DAO led to the theft of $60 million worth of Ether.

bZx Exploits: In 2020, the bZx protocol suffered multiple attacks due to smart contract vulnerabilities, resulting in significant losses.

Mitigation Strategies:

Rigorous Auditing: Regular and thorough audits by reputable security firms.

Bug Bounties: Incentivizing the community to identify and report vulnerabilities.

Formal Verification: Using mathematical methods to prove the correctness of smart contracts.

Regulatory and Legal Challenges

Compliance Issues

DeFi operates in a largely unregulated space, which presents challenges in terms of compliance with existing financial regulations.

Key Points:

AML/KYC Requirements: Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations are difficult to enforce in a decentralized environment.

Jurisdictional Differences: DeFi platforms operate globally, but financial regulations vary by country, creating compliance complexities.

Consequences:

Regulatory Crackdowns: Platforms that fail to comply with regulations risk being shut down or facing legal action.

User Impact: Users may face restrictions or penalties for using non-compliant platforms.

Mitigation Strategies:

Self-Regulation: Industry standards and best practices for compliance.

Hybrid Models: Combining decentralized and centralized elements to meet regulatory requirements.

Legal Uncertainties

The legal status of DeFi projects and the enforceability of smart contracts are often unclear, leading to uncertainties and potential legal disputes.

Key Points:

Contract Enforceability: The legal recognition of smart contracts varies by jurisdiction.

Regulatory Evolution: Rapid changes in regulations can create uncertainty for DeFi projects.

Consequences:

Legal Risks: Uncertain legal frameworks can lead to disputes and challenges in enforcing agreements.

Innovation Stifling: Fear of regulatory backlash may deter innovation and development in the DeFi space.

Mitigation Strategies:

Legal Counsel: Engaging legal experts to navigate regulatory landscapes.

Proactive Engagement: Working with regulators to shape favorable policies and frameworks.

Market Volatility and Financial Risks

DeFi platforms are exposed to the inherent volatility of the cryptocurrency market, which can lead to significant financial risks for users.

Key Points:

Price Volatility: Rapid price fluctuations of cryptocurrencies can impact collateralized loans and liquidity pools.

Liquidation Risks: Over-collateralized loans are subject to liquidation if collateral values drop below a certain threshold.

Impermanent Loss: Liquidity providers can experience losses due to changes in the value of assets in liquidity pools.

Examples:

March 2020 Crash: The sudden market crash led to massive liquidations on platforms like MakerDAO.

Impermanent Loss: Users providing liquidity to AMMs can face losses when the price of deposited assets diverges significantly.

Mitigation Strategies:

Risk Management Tools: Utilizing hedging strategies and insurance products.

Diversification: Spreading investments across multiple assets and platforms.

Stablecoin Use: Using stablecoins to mitigate exposure to volatility.

Scalability and Interoperability Issues

Scalability and interoperability are significant technical challenges facing DeFi platforms, impacting their performance and user experience.

Key Points:

Scalability: Current blockchain networks, particularly Ethereum, face limitations in transaction throughput and speed, leading to congestion and high fees during peak times.

Interoperability: DeFi platforms often operate in isolation, with limited ability to interact with other blockchains and financial systems.

Consequences:

User Frustration: High fees and slow transaction times can deter users.

Limited Functionality: Lack of interoperability restricts the potential for integrating various DeFi services.

Mitigation Strategies:

Layer 2 Solutions: Implementing off-chain scaling solutions to increase transaction throughput and reduce costs.

Cross-Chain Bridges: Developing protocols that enable seamless interaction between different blockchains.

Alternative Blockchains: Utilizing blockchains with higher scalability, such as Binance Smart Chain or Polkadot.

In summary, while DeFi offers transformative potential for financial services, it also presents significant challenges and risks. Addressing technical vulnerabilities, navigating regulatory landscapes, managing financial risks, and improving scalability and interoperability are crucial for the sustainable growth of the DeFi ecosystem.

VII. Case Studies and Real-world Applications

Successful DeFi Projects and Platforms

MakerDAO and DAI Stablecoin

MakerDAO is one of the most prominent and successful DeFi projects, known for creating the DAI stablecoin. DAI is a decentralized, collateral-backed stablecoin pegged to the US Dollar. MakerDAO uses a system of smart contracts on the Ethereum blockchain to maintain the stability of DAI through over-collateralization and automated governance.

Key Features:

Collateralization: Users lock up cryptocurrencies like Ether (ETH) in MakerDAO's smart contracts to generate DAI.

Stability Mechanism: The stability of DAI is maintained through dynamic interest rates and automated liquidation mechanisms.

Decentralized Governance: MakerDAO token holders participate in governance decisions, including changes to the collateralization ratio and stability fees.

Impact:

Stable Medium of Exchange: DAI provides a stable currency option in the volatile cryptocurrency market.

Financial Tools: Enables borrowing and lending without the need for traditional banks, enhancing financial accessibility.

Innovation: Pioneered the concept of algorithmic stablecoins, influencing numerous other projects in the DeFi space.

Real-World Example:

Venezuela: In hyperinflationary environments like Venezuela, DAI has provided a stable store of value and medium of exchange for residents facing severe currency devaluation.

Uniswap and Decentralized Trading

Uniswap is a leading decentralized exchange (DEX) that allows users to trade cryptocurrencies directly from their wallets without relying on a central authority. It uses an automated market maker (AMM) model to facilitate trading and liquidity provision.

Key Features:

Automated Market Maker (AMM): Liquidity pools are created by users who deposit pairs of tokens. Prices are determined by a mathematical formula based on the ratio of tokens in the pool.

Permissionless Trading: Anyone can trade tokens on Uniswap or create new trading pairs without needing approval.

Liquidity Provider Rewards: Users who provide liquidity to the pools earn a share of the trading fees.

Impact:

Accessibility: Uniswap enables anyone to trade tokens without needing to go through a centralized exchange, democratizing access to trading.

Innovation: Introduced the AMM model, which has been widely adopted and adapted by other DeFi projects.

Volume: Uniswap regularly achieves high trading volumes, rivaling those of major centralized exchanges.

Real-World Example:

NFT Trading: Uniswap has been used for trading NFT-related tokens, providing liquidity and price discovery for digital art and collectibles.

Real-World Impact and User Stories

Financial Inclusion Examples

DeFi has made significant strides in promoting financial inclusion by providing financial services to underserved populations.

Examples:

Microloans in Developing Countries: Platforms like Aave and Compound have enabled users in developing countries to access microloans without needing traditional credit scores or banking relationships.

Remittances: DeFi platforms have facilitated cheaper and faster cross-border remittances, helping migrant workers send money home with lower fees and quicker settlement times.

User Stories:

Kenya: Farmers in Kenya have used DeFi lending platforms to access small loans for purchasing seeds and equipment, boosting agricultural productivity and incomes.

Philippines: Filipino workers abroad have utilized DeFi platforms for remittances, reducing the cost and increasing the speed of sending money to their families.

Innovations in Emerging Markets

Emerging markets have been fertile ground for DeFi innovations, addressing unique challenges and unlocking new opportunities.

Examples:

Tokenization of Assets: Projects in regions like Latin America have experimented with tokenizing real estate and agricultural products, enabling fractional ownership and improving access to investment opportunities.

Decentralized Identity: DeFi projects are working on decentralized identity solutions to provide verifiable digital identities for individuals without traditional documentation, facilitating access to financial services.

User Stories:

India: Small businesses in India have used DeFi platforms for crowdfunding and peer-to-peer lending, bypassing the complexities and inefficiencies of traditional banking systems.

Nigeria: DeFi has enabled Nigerians to hedge against local currency depreciation by holding stablecoins and accessing global financial markets.

In summary, successful DeFi projects like MakerDAO and Uniswap showcase the potential of decentralized finance to revolutionize traditional financial services. Real-world applications and user stories highlight the tangible impact of DeFi in promoting financial inclusion and driving innovation in emerging markets.

VIII. Future of DeFi and Blockchain in Financial Services

Potential Developments and Innovations

Cross-Chain Interoperability

Cross-chain interoperability refers to the ability of different blockchain networks to communicate and interact with each other. This development is crucial for the growth and integration of DeFi ecosystems.

Key Points:

Interoperability Protocols: Technologies such as Polkadot, Cosmos, and Chainlink aim to enable seamless interactions between various blockchain networks.

Bridges and Hubs: These platforms create bridges that allow tokens and data to move freely across chains, fostering collaboration and resource sharing.

Benefits:

Enhanced Liquidity: Cross-chain solutions can aggregate liquidity from multiple blockchains, improving market depth and reducing fragmentation.

Unified Ecosystem: Users can access services and assets from different blockchains through a single interface, simplifying the user experience.

Innovation and Flexibility: Developers can leverage the unique features of various blockchains to build more robust and versatile DeFi applications.

Examples:

Polkadot: Aims to connect multiple specialized blockchains into a unified network, facilitating interoperability and shared security.

Cosmos: Provides an ecosystem of connected blockchains that can scale and interoperate with each other.

Integration with Traditional Finance

Integrating DeFi with traditional finance (TradFi) can create a more inclusive and efficient financial system by combining the strengths of both sectors.

Key Points:

Hybrid Solutions: Projects that blend decentralized and centralized elements to meet regulatory requirements and provide a smoother transition for traditional financial institutions.

Institutional Adoption: Increasing interest from banks, hedge funds, and other financial institutions in DeFi technologies and products.

Benefits:

Broader Access: Traditional financial institutions can leverage DeFi innovations to offer new products and services to their clients.

Enhanced Trust: Combining the transparency and efficiency of DeFi with the established reputation of traditional finance can build trust among users.

Regulatory Compliance: Hybrid models can help address compliance issues, making it easier for DeFi platforms to operate within existing legal frameworks.

Examples:

JPMorgan's Onyx: A blockchain-based platform for wholesale payments that integrates aspects of DeFi.

Aave Arc: A permissioned DeFi platform designed for institutions to access decentralized lending and borrowing within a compliant framework.

Predictions and Trends

Growth Projections

The DeFi market is expected to continue its rapid growth, driven by technological advancements, increased adoption, and expanding use cases.

Key Points:

Market Size: The total value locked (TVL) in DeFi protocols is projected to grow significantly, with more assets and users entering the ecosystem.

User Base: The number of DeFi users is expected to increase as awareness and accessibility improve.

Drivers of Growth:

Technological Innovation: Advances in blockchain technology, scalability solutions, and user-friendly interfaces.

Institutional Interest: Growing participation from traditional financial institutions and large-scale investors.

Global Reach: Expansion into emerging markets and regions with limited access to traditional financial services.

Examples:

TVL Projections: Analysts predict the DeFi market could reach hundreds of billions of dollars in TVL within the next few years.

User Growth: Platforms like MetaMask have seen exponential growth in user adoption, indicating a rising interest in DeFi.

Evolving Regulatory Landscape

The regulatory environment for DeFi is expected to evolve, with governments and regulatory bodies developing frameworks to address the unique challenges posed by decentralized finance.

Key Points:

Regulatory Clarity: Clear guidelines and regulations will emerge, helping DeFi projects navigate legal requirements and reduce uncertainty.

Global Coordination: International cooperation among regulatory bodies to create harmonized standards for DeFi.

Impact on DeFi:

Compliance Requirements: DeFi platforms may need to implement measures to comply with KYC, AML, and other regulatory standards.

Innovation Incentives: Regulatory clarity can encourage innovation by providing a more predictable and stable environment for development.

Examples:

US SEC and CFTC: These agencies are actively exploring ways to regulate DeFi activities to protect investors and ensure market integrity.

European Union: The EU is working on the Markets in Crypto-Assets (MiCA) regulation, which aims to create a comprehensive framework for digital assets, including DeFi.

In summary, the future of DeFi and blockchain in financial services looks promising, with potential developments in cross-chain interoperability and integration with traditional finance driving innovation and growth. However, the evolving regulatory landscape will play a critical role in shaping the trajectory of DeFi, balancing the need for compliance with the desire for innovation and inclusivity.

IX. Conclusion

DeFi and Blockchain's impact on financial services includes understanding concepts, advantages, challenges, and real-world applications. DeFi transforms financial services by removing intermediaries, reducing costs, and enhancing security. It promotes financial inclusion and innovation, democratizing finance for underserved populations. The future of DeFi entails growth, innovation, cross-chain interoperability, regulatory integration, and a potential global financial revolution. Sustainable development and widespread adoption require addressing risks and challenges in the evolving DeFi ecosystem.

X. References and Further Reading

Academic Papers and Articles

Buterin, V. (2013). "Ethereum Whitepaper: A Next-Generation Smart Contract and Decentralized Application Platform."

Schär, F. (2021). "Decentralized Finance: On Blockchain- and Smart Contract-Based Financial Markets." Federal Reserve Bank of St. Louis Review.

Werbach, K. (2018). "The Blockchain and the New Architecture of Trust." MIT Press.

Industry Reports and Whitepapers

"DeFi Beyond the Hype: The Emerging World of Decentralized Finance." (2020). World Economic Forum.

Ethereum.org - Resources and information on Ethereum and its ecosystem.

Free Consultation for Blockchain Financial services

Infiniticube offers free consultation on all the services mentioned above, providing expert guidance and support to help your business harness the full potential of DeFi solutions.

Ready to transform your financial services with DeFi? Click the button below to get started!

He is working with infiniticube as a Digital Marketing Specialist. He has over 3 years of experience in Digital Marketing. He worked on multiple challenging assignments.

Our newsletter is finely tuned to your interests, offering insights into AI-powered solutions, blockchain advancements, and more. Subscribe now to stay informed and at the forefront of industry developments.

June 27, 2025

June 27, 2025

Balbir Kumar Singh

Balbir Kumar Singh

0

0