2020 was not the finest period for several businesses because of COVID-19. But certainly, the likes of Fintech recorded a rapid improvement in the pandemic’s course.

Without physical contact, consumers counted on online financial help to access and distribute funds and Fintech solutions made it through.

The reputation of Fintech has peaked lately, with 96% of international users agreeing to be mindful of a minimum of one Fintech service.

Let’s look at some Fintech trends that are predicted to determine financial services in 2025.

#1 The Dispute of Small Businesses Moves Up/Down the Supply Chain

2020 witnessed three noteworthy advancements in the battle for small business relationships:

1) PPP Loan Paycheck Protection Program is necessary because it facilitates several mid-size and other minor banks and credit unions to lend some money to small businesses that are ignored or turned their back by the leading banks where these businesses maintain their deposit accounts.

2) Goldman Sachs/Amazon Partnership Amazon eventually unlocked the gate to third parties to quickly lend to the platform’s vendors. It’s a decisive step because Amazon released $1 billion in merchant cash speeds up to its merchants’ handful of years ago.

3) Stripe Announcement for Stripe Treasury

Result #1 was significant for several mid-sized financial systems because it allowed them straightforward entry to a unique set of likely consumers. But if the small businesses engaged are Amazon merchants or Stripe consumers, that direct connection is trivial.

Amazon’s and Stripe’s capability to install banking services into their current services allows those firms and their associates considerable leverage because they have successful access to data about those merchants.

Is that the end?

Not entirely!

Functions at the beginning of the value chain like production, supply management, payouts, etc. — and after payouts in the value chain such as invoicing, accounts receivable, etc., are unnoticed by Amazon, Stripe, and Square.

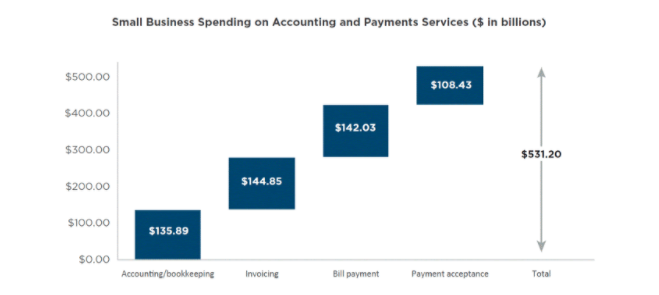

As per a survey of small businesses by Cornerstone Advisors, small businesses approve 11 types of payment — the majority of those payments are not delivered by Stripe or Square.

As reported by Cornerstone’s study, small businesses invest over $500 billion in accounting, invoicing, bill payment, and payment acceptance services from third-parties.

SOURCE: CORNERSTONE ADVISORS SURVEY OF 1,265 SMALL BUSINESS OWNERS AND EXECUTIVES, Q1 2020

Several small businesses would think of getting accounting and payments services from a bank — as would several other banks that don’t presently use third-party services and incur internal charges for their accounting and payments activities.

To rival Amazon, Stripe, and Square, we must embed financial institutions into small businesses’ value chains.

#2 Autonomous Finance

Autonomous finance is first on the list of notable Fintech novelties. Manipulating work with service payout settlements, coverage, cable subscriptions, etc., can be staggering.

Autonomous finance lifts the burden off customers’ shoulders and computerizes the monetary decision-making procedure with Artificial Intelligence (AI) and Machine Learning.

As several people try to set up a better time for themselves, they will hand over repeated activities to Fintech solutions.

#3 Digital Banking

Still, as more people restrain themselves in their homes, the need to visit offline organizations has, unsurprisingly, declined.

With more powerful advancements carried out in artificial intelligence (AI), biometrics, open banking, and cybersecurity, digital banking is easier than ever, with users now in a position to access an ample variety of personal financial reports and perform essential activities with only a few clicks of your smartphones.

A Boston Consulting Group (BCG) study in 15 countries reported in May discovered that a substantial 44 percent of 18 to 34-year-olds had registered in online or mobile banking for the first time at the time of the COVID-19 emergency.

With the increasing usage of digital banking, we should also pay attention to the parallel drop in paper-based banking. The pandemic has undoubtedly sped up the transformation towards a paperless world, and with consumers getting more relaxed, clients are reaching out to their banks via apps and online messaging — and completing transactions. We are going to see that digital banking will perform even better in 2021.

#4 Micro-Lenders Will Mushroom

As life is gradually picking up the pace and lockdowns being lifted, the business activities come back to pre-COVID-19 levels, thanks to the impending influx of vaccines, the lending schemes are hopeful of picking up, notably as small merchants aim to overhaul their activities.

The rise in hiring work is also about encouraging loans as expenditure levels standardize, compelling firms to match rising demand. This will presumably cause micro-lending startups to support small businesses and personal loans instantly and digitally with banks.

Quick processing times will encourage organizations to get on track sooner while computerizing loan demands and disbursals that will benefit many people to apply for loans.

#5 Customer-Centric Applications

The expansion of Fintech solutions has led consumers to the fore of every financial institutions’ plans. Once upon a time these financial industries shaped processes and applications to satisfy their own demands, today they should focus on addressing a top-quality customer experience if they prefer to stay ambitious in a teeming flea market.

The procedure usually starts with cutting resistance wherever possible to support end-users to get the work and services they need. With consumers interacting more and more with financial enterprises across multiple mediums, Fintech developers should develop solutions that reinforce those relationships and develop their capacity.

Excluding manual procedures, minimizing external software reliance, and automating recurring activities will remain a focal point of significance for Fintech applications.

Consumers no longer have the endurance to regularly complete lengthy forms or undergo the depressing procedure of downloading, photocopying, signing, and scanning forms.

#6 Financial Literacy

Customer financial literacy levels will impact their finances either positively or negatively. As per a Bankrate report, an ordinary American family has $8,863 in bank savings.

The younger generation has even lesser savings. Along the same lines, 55% of interviewees in a new survey admitted they lack satisfactory finances for their demands. Conditions would reasonably be different if customers were better educated about their funds.

Fintech solutions are a powerful means for financial literacy. With a compilation of big data, users with poor finances can gain insights into finances. Fintech tools can educate consumers with the financial information to carry out reasonable financial judgments.

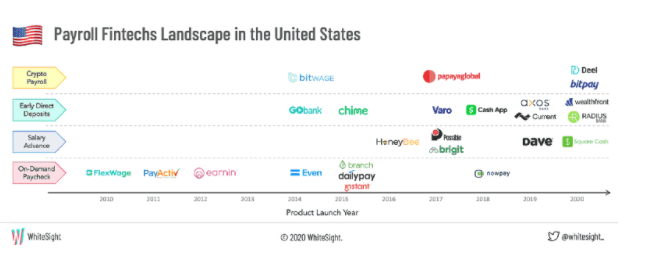

#7 Finally Payroll Fintech Received Some Attention

WhiteSight describes four divisions in the payroll Fintech space:

1) Salary On-demand Fintechs in this division are associated with enterprises, HR software providers, and payroll systems to set up smooth access to earned salaries.

2) Salary Advance Fintechs in this group grant interim credit to working staff according to their payroll and escape the outrageous rates imposed by payday lenders.

3) Early Direct Deposit This aspect, mostly given by challenger banks, permits bank account holders to get payroll up to two days before regular payday.

4) Crypto Payroll This is the latest division that permits organizations to make salary payrolls through various crypto-currencies.

SOURCE: WHITESIGHT

Supporters of payroll Fintech usually speak about these services from a financial well-being angle, but much like the small business clash, payroll Fintech is indeed striving to advance the deposits and disbursements value chain.

ADP, a large payroll provider, striving for years to expand its links with users who receive paychecks from them. It is surprising that Big Tech organizations have gained no payroll providers yet.

In the future, payroll Fintech is going to draw more attention in 2025.

Solve Your Fintech Challenges

Our group of Fintech experts will help you in finding Fintech solutions that require; therefore, you can satisfy the demands of 2025 and further.

Digital Marketing Specialist at Infiniticube, a leading app development and digital marketing agency in India. I specialize in B2B lead generation, AI-driven marketing solutions, and blockchain technology. Follow along for actionable insights on software trends and digital growth strategies for 2025 and beyond.

Our newsletter is finely tuned to your interests, offering insights into AI-powered solutions, blockchain advancements, and more. Subscribe now to stay informed and at the forefront of industry developments.

June 27, 2025

June 27, 2025

Balbir Kumar Singh

Balbir Kumar Singh

1

1

This article opened my eyes, I can feel your mood, your thoughts, it seems very wonderful. I hope to see more articles like this. thanks for sharing.